What happened

In March 2026, China shipped a record 68 gigawatts of solar products (modules, cells and wafers) in a single month, equivalent to Spain’s entire installed capacity. The ongoing conflict in the Gulf had disrupted the Strait of Hormuz and sent oil prices surging, triggering a global scramble for renewables. Buyers turned to the only supplier capable of delivering at that scale.

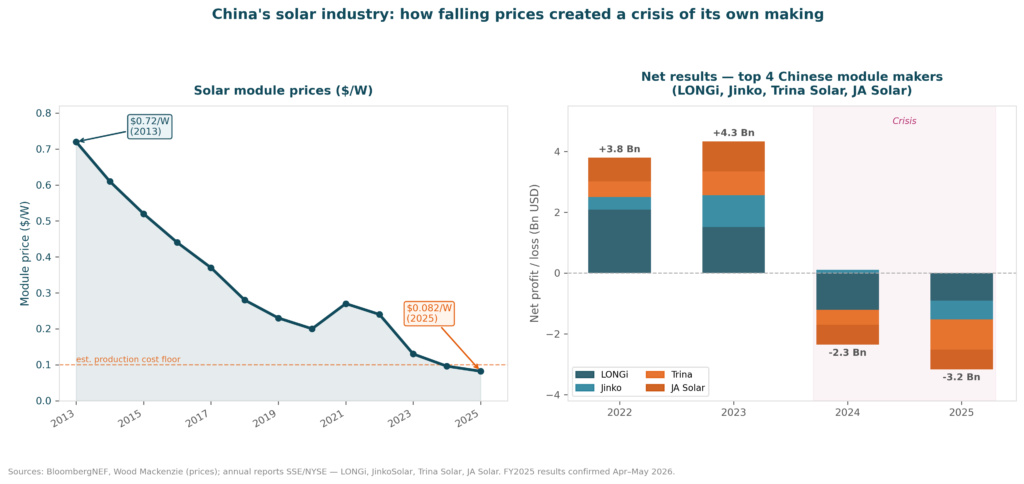

Yet China’s four leading module manufacturers (LONGi, Jinko, Trina Solar, JA Solar) had accumulated more than $3 billion in losses across 2025. Revenue was rising. Margins had ceased to exist.

Sources: BloombergNEF, Wood Mackenzie; annual reports SSE/NYSE — LONGi, JinkoSolar, Trina Solar, JA Solar. FY2025 results confirmed Apr.–May 2026.

Why it matters

The situation in China is a textbook illustration of a paradox the Fundamental on the Energy Transition maps precisely: the solar learning curve worked too well.

Since 2013, the price of photovoltaic modules has fallen by more than 88%, from $0.72/W to under $0.10/W. That collapse made solar the cheapest new source of electricity on earth. It also produced a structural overcapacity without precedent: China can now manufacture roughly 1,200 GW of panels per year against a global demand estimated at between 650 and 700 GW depending on the agency.

The consequences are visible across the industry. Factories are running at 40 to 60% of capacity. Sale prices sit below production costs. Since 2024, more than forty companies in the supply chain have been delisted, acquired or gone bankrupt (CPIA/Reuters). LONGi, one of the two largest module manufacturers in the world alongside Jinko, swung from a $1.5 billion profit in 2023 to a $900 million loss two years later.

The Hormuz paradox. The rush toward Chinese solar products was real: exports doubled in a month. But the manufacturers themselves concede it changes nothing structurally. An industry executive cited by Reuters put it plainly: “The capacity is still there. It hasn’t been shut down.”

Beijing attempted an industrial response: a $7 billion consolidation fund, backed by the six largest polysilicon producers, was designed to shut down a third of excess capacity. China’s antitrust regulator (SAMR) suspended the plan in January 2026, citing cartel concerns. The sector’s restructuring has no operational mechanism.

What has produced concrete effects is the cancellation of China’s 13% export VAT rebate in late 2025. Module prices rose by roughly 9% in the fourth quarter of 2025 (Wood Mackenzie), driven by that policy shift and upstream production cuts. This is not a demand recovery. It is the end of an era of artificially low prices.

The end of the era of historically cheap panels may already be here. For solar projects around the world, 2024 may look, in hindsight, like the all-time low.

To understand how a technology can command 80% of a global market and still bleed money, read the Fundamental “The Energy Transition.”

Read the Fundamental →Sources and References

─────────────────────────────────────────────

Article by The Foundations – The fundamentals behind the headlines

India’s Demographic Shift

Demographic Transition: Aging, Fertility and Consequences

Alphabet raises $80 billion to fund AI

International Migration: Flows, Causes and Impact

China makes 80% of the world’s solar panels. And is losing billions.